For millions of us, Amazon long ago replaced the high street as the first port of call for everything from books and consumer gadgets to DVDs and digital content.

The company has it all, and at low prices; it’s so big it’s almost synonymous with online shopping – yet somehow this global behemoth still fails to make ends meet.

The company’s focus on winning customers through ever-lower prices has, on the face of it, been a success. Last year’s company results showed revenues of $48 billion, which, if it were a country, would nestle Amazon neatly between the GDP of Slovenia and Guatemala.

If you looked at Amazon financially and you didn’t know what it did, you wouldn’t want to own it

Yet in its latest quarterly figures, the company recorded a loss of $274 million on earnings of $13 billion. Heavy spending on Kindle hardware has led to higher costs, even as it has emerged that the company paid woefully little in UK taxes.

A flood of negative publicity has opened Amazon up to further questions over how it could possibly fail to make money when paying minimal sales tax in so many jurisdictions. Could it be that Amazon’s business model is fundamentally flawed?

“$50 billion start-up”

The Amazon model – an online version of stack ’em high, sell ’em cheap – has been brilliant in growing its customer base. The problem for investors in the company is that the constant push into new markets makes it difficult to assess its real value.

“Amazon doesn’t disclose its margins, so we’re flying blind,” says Lawrence Haverty, a portfolio manager with publishing and media investment company Gabelli Multimedia Trust. “If you looked at Amazon financially and you didn’t know what it did, you wouldn’t want to own it. It makes a very inadequate return on investment capital.”

Amazon’s latest results

Amazon’s shares soar despite $39m annual loss

Haverty believes Amazon makes such thin margins on its huge inventory that there’s little wonder the business isn’t making money in many of its activities, which now range from retail and cloud hosting to hardware and platform design with its Kindle range.

“It’s hard to conclude that in any of its non-cloud businesses it makes anything resembling an economic profit,” he says. “The market doesn’t hold [CEO] Jeff Bezos accountable to earn a competitive return – it gives Amazon a free pass to get into these markets with a very low margin structure and then do something else.”

Haverty suspects that, considering how Amazon is running its business, the company isn’t ever going to make enough of a profit to justify its stock price. “Right now this is a $50 billion start-up – it isn’t making a return against $50 billion of volume.”

From the consumer’s point of view this is all good news, but retailers are normally in business to make money. According to analysis from investment house Qineqt, over the past five years Amazon has traded at profit margins of 2.72% – slim, but acceptable given the scale of the operation. In the past year, however, that margin has tumbled to 0.69%.

Buying into the Kindle

Instead of raising the prices of its products to increase profit, Amazon has focused on entering new markets. Much of the recent decline in profits can be put down to its investment in the Kindle. But even after this investment, the company has made it clear it doesn’t expect to make money from the hardware, preferring again to focus on new customers.

“Our approach is to work hard to charge less,” said Bezos in the recent company statement. “Sell devices near break-even and you can pack a lot of sophisticated hardware at a very low price point. Our approach is working – the $199 Kindle Fire HD is the best-selling product across Amazon worldwide.”

The problem? Amazon makes nothing from those sales; in fact, analysts believe the company is making a loss. The model follows the Gillette school of marketing by which you sell razors for next to nothing in the expectation of making money on replacement blades.

In Amazon’s vision, Kindle ebook sales and other content on its Fire tablets will recoup the investment in subsidised hardware – but there remains a suspicion that the company isn’t making much on that content either.

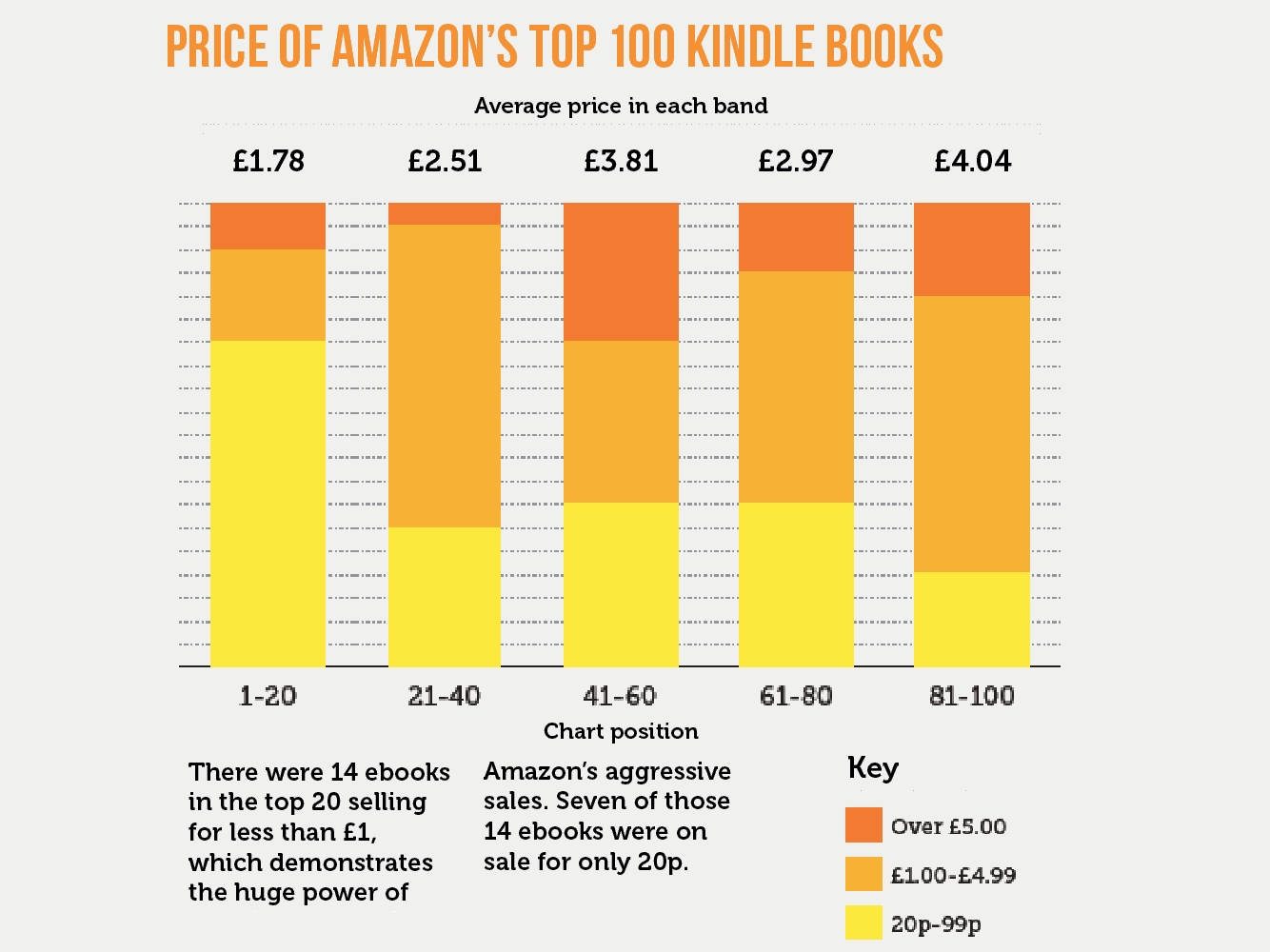

In a trawl of Amazon’s top 20 best-selling ebooks for the Kindle, the average price was only £1.78; seven of those cost a ridiculous 20p.

Whatever the split between Amazon and the publisher in each case, the company will be making mere pennies after administration, distribution and platform costs. This aggressive tactic may be working to increase sales, according to experts, even though it could prove costly in the short term.

“People that buy a Kindle as their starter for digital books are going to build their entire libraries around that ecosystem,” says Joe Magyer, an Amazon specialist and senior analyst at The Motley Fool, a financial services company. “If you buy into it, you’re likely to stick with Amazon, and that will serve it well over the long term; it could be a good investment even though it’s killing gross margins. Amazon has to balance the razor and the blades; if you sell the razor at break-even or at a loss, and people don’t come back and buy the blades, then you’re not doing well.”

Even Amazon accepts it may struggle to sell its new platform at a profit, and that it can’t be sure customers will come back to fill their devices with videos, music and books.

“We may have limited or no experience in our newer market segments, and our customers may not adopt our new offerings. These offerings may present new and difficult technology challenges,” the company warned in its 2011 results statement. “In addition, profitability, if any, in our newer activities may be lower than in our older activities, and we may not be successful enough in these newer activities to recoup our investments in them.”

According to analysts, Amazon is trying to use subsidised hardware and cheap ebooks to squeeze Apple into lowering its prices to match. It’s a bold gamble given Apple’s healthy bank balance and user base.

Amazon and Google are trying to kill the economics for the other hardware guys

“Both Amazon and Google are in a good position because they don’t need to make money on the hardware, and that’s a good thing in the long term because making money in consumer electronics hardware is incredibly difficult,” says Magyer. “Amazon and Google are trying to kill the economics for the other hardware guys. Amazon can’t make good margins while trying to ruin it for Apple by making it scrimp on margins.”

However, a brief look at Apple’s results for the same quarter in which Amazon made that $274 million loss highlights the difference that can be made by a solid margin on hardware and a ready supply of content. With Apple’s iPad mini starting at £269, compared to the basic Kindle Fire at £129, Apple is making good money on each device – something that contributed towards the company’s $8.2 billion in profits for the quarter.

It isn’t yet clear whether Amazon’s content deals established in the UK for films and television will make a better contribution to its bottom line than ebooks.

The DRM threat

Although literature on the bestsellers list is cheap – probably because dirt-cheap books sell more copies – well-known books are often more expensive on Kindle than hardback, which makes little sense to consumers. There’s little point in buying into the ebook ethos if the titles you really want to buy are cheaper in print form.

And once you have bought into the Kindle, it isn’t easy to buy content from elsewhere, with the company using DRM controls and occasionally exercising its ability to remove content that falls foul of its terms and conditions.

Amazon scored a PR own goal in October by removing content from a user’s device, claiming the Norwegian woman had bought the content while a linked account was being used improperly.

Review

As media commentator Martin Bekkelund said in a blog that went viral and provoked widespread criticism of Amazon: “This shows the very worst of DRM. If Amazon thinks you’re a crook, it will throw you out and take away everything that you’ve bought. And if you disagree, you’re totally outlawed. With DRM, you don’t buy and own books, you merely rent them for as long as the retailer finds it convenient.”

People who grew up buying books were, not surprisingly, miffed when Amazon’s “rental” model raised its head. With rivals such as Kobo proving far more flexible, Amazon’s tight control could backfire. Apple was eventually forced to remove DRM from its iTunes tracks to keep customers happy; repeating such a move on the cheap Kindle could prove costly.

Taxing issues

Amazon is just one of many global corporations well versed in making the most of international tax systems to pay as little as possible in UK taxes. But the fuss isn’t restricted to these shores.

“Amazon has been given an advantage by the [US] government because, until recently, it hasn’t had to pay sales tax on what it sells – and it still isn’t making a profit,” says Haverty.

Amazon maintains that it pays the taxes it’s required to by law, but scrutiny into such corporate practices is growing. If governments seek to close the exploited regulations, Amazon stands to lose one of its key competitive advantages – something to which the company readily admits.

“During the ordinary course of business, there are many transactions for which the ultimate tax determination is uncertain,” Amazon told investors in recent statements. “We are subject to audit in various jurisdictions, and such jurisdictions may assess additional income tax liabilities against us.”

Reputation damage

While the favourable tax position may remain and make it easier for Amazon to turn a profit, the reputational damage is harder to assess, with UK companies protesting: a media storm saw many headlines echoing The Guardian’s “Amazon: £7bn sales, no UK corporation tax”.

Find out more

According to British retailers, the 27% tax they pay is money that could be invested in their future, through lower prices to attract more customers or through better distribution systems. They are at a disadvantage compared to Amazon.

“If you’re giving 27% of your profits to the exchequer, rather than being domiciled in a tax haven and having much more, you’ll be out-invested and ultimately out-traded,” Andy Street, CEO of John Lewis, told Sky News.

Yet although the UK’s independent booksellers have tried to cash in on Amazon’s bad publicity by launching a “we pay our taxes” campaign, it’s unclear whether it will have any impact. According to the TaxPayers’ Alliance, it’s seen only marginal support for boycotting Amazon because it remains the cheapest source for many goods.

“People we’ve spoken to are more concerned about the loopholes in the system than any company,” said a spokesperson. “I’ve seen a few comments about people buying from elsewhere; at the moment people are hard-pressed, with high costs of living, so if they can save a few bob when they’re doing their shopping, they’ll continue to do so.”

In addition, Amazon has alienated some authors and publishers with its pricing strategy, publishing books below cost price. For example, when Ken Follett’s Winter of the World went on sale at 20p instead of its recommended price of £11.64, his agent Al Zuckerman branded it “absurd and outrageous”.

People we’ve spoken to are more concerned about the loopholes in the system than any company

However, in a vignette that highlights that even if it isn’t profitable, Amazon remains hugely influential, the agent later chose not to elaborate when we contacted him. “It’s too ticklish a subject,” said Zuckerman. “I don’t want to comment on this because we have too many authors whose livelihoods depend on Amazon.”

The future?

Without allies in its key markets, Amazon could find itself increasingly marginalised. There are no administrators circling yet, but the fact remains that a company with such an enormous customer base should be making money, more so given the advantages it has over rivals, both online and in the UK.

Right now it’s moving from market to market using aggressive pricing to entice more customers, but at some point it will have to focus on making money. Otherwise, when there are no more users to entice, Amazon might find it can’t run a successful business with the ones it has.

Disclaimer: Some pages on this site may include an affiliate link. This does not effect our editorial in any way.